Since the bursting of the U.S. housing bubble in 2005, the billion dollar bailouts of “banks too big to fail,” and the “Great Recession” of 2007 that stalled the U.S. economy and helped decimate the economies of some countries, it appears we have once again escaped a financial apocalypse.

As of 2013 the number of total U.S. home foreclosures has fallen, housing prices and employment are rising, the stock market has passed an historical benchmark of 16,000. Thanks to various housing assistance programs, some people who would have lost their homes have been spared.

One sobering reality, however, remains unchanged. Much of the defective institutional machinery and misguided policies that helped create the global financial crisis — e.g., the repeal of Glass-Steagall (which dismantled an essential wall of separation between commercial and investment banking functions); the criminal disregard of lending standards; the securitization of sub-prime mortgages — is still intact. The Federal Reserve continues its policy of “quantitative easing,” pumping up the money supply by buying up not only more federal debt but securitized mortgages as well. And yet, the economy (in the U.S. and abroad) seems no closer to a healthy rate of growth needed to raise the real purchasing power of the average citizen.

Clearly what is needed is not simply more patchwork and quick-fixes, but a radical overhaul of our mortgage and financing institutions in order to prevent another, even more disastrous global financial collapse. We need to ask once again, and with minds open to new solutions, if there is a financially viable plan that would save homeowners at risk of foreclosure because of bad loans? Is there a non-inflationary, free market alternative to today’s misuse of the Federal Reserve’s power in financing government bailouts of “too big to fail” banks, Wall Street securities dealers and predatory mortgage loan sharks?

This concept paper proposes a way of solving the continuing housing foreclosure crisis in local communities, and ultimately providing a financially sound means for all Americans to have access to reasonably-priced housing in a way that builds their personal equity rather than burying them in perpetual debt.

The Homeowners Equity Corporation:

An Economic Empowerment Tool for Solving the Foreclosure Crisis

The Homeowners Equity Corporation (HEC) is a for-profit stock corporation that purchases foreclosed residential properties in a local community, and through a “lease-to-equity” arrangement enables homeowners facing foreclosure to: 1) remain in their residence, 2) pay off the market cost of the residence, and 3) build up equity as shareholders of the HEC.

The HEC allows citizens to escape from the worst form of credit (loans for consumer goods that don’t pay for themselves and are made to people who can’t repay the loans) to the best form of credit (loans to purchase capital assets that pay for themselves and that turn non-owners into owners of income-producing assets). The HEC is based on a new monetary and tax approach that promotes the financing of private sector capital formation in ways that create new owners of that growth and thereby spread purchasing power throughout the economy.

One of the key characteristics of the Homeowners’ Equity Corporation is that it minimizes risks of the resident-shareholder foreclosing on the home mortgage by acting as a form of capital credit “insurance,” through pooling of risk. There will always be a certain percentage of homes that are unoccupied for a time, but the shareholder’s equity will be based on a HEC’s value per share, based in turn on the aggregate value of all homes owned by a HEC, not the value of the home occupied. Also, a HEC’s value per share will depend in part on the occupancy rate of all homes, as will the payments on the loans used by the HEC to acquire the homes. It is obviously much easier to make payments on 100 houses, of which 90 are occupied and generating rent payments, than on a single house with no rent payments coming in.

The HEC also provides a means for those who cannot afford monthly lease payments on their home, to participate in the lease-to-equity program. Vouchers linked to need (for a specified amount of time) could be provided. For example, 25% of a HEC resident-shareholder’s income would go to cover housing leases. The amount of the voucher to supplement this would be the difference between the homeowner’s total income and the monthly lease payments. To protect against people playing the system, there would need to be a limit on how much of a voucher someone could receive and for how long they could receive a voucher to remain in a particular residence owned by the HEC.

Advantages of the Homeowners Equity Corporation

For the resident-shareholder:

- Protects homeowners from losing their primary residence because of a bad loan.

- Saves homes of people in foreclosure, in danger of foreclosure, or who have given a deed in lieu of foreclosure.

- Allows the former owners of houses that have been foreclosed to acquire full voting, full dividend payout shares in a Homeowners Equity Corporation that holds title to their homes.

- Makes it much easier for homeowners to “sell” their homes by cashing in their equity shares. It is up to the Homeowners’ Equity Corporation to find a new tenant, not the resident’s problem to find a buyer.

- Allows tax deductibility of both principal and interest payments on acquisition loans at the corporate level.

- Allows tax deductibility of dividend payments (actually rebates of rent payments in excess of the company’s needs).

- The HEC could provide upkeep services (similar to a condominium association) to homeowners in the HEC, allowing for economies of scale to bring down the cost of yard maintenance and home repair.

For the lender:

- Allows lenders to recoup a greater percentage of their bad loans.

- Allows lenders to sell foreclosed properties at market value.

- Spreads risk among many homebuyers and reduces insurance premiums.

For the local community:

- Creates a more stable housing market less subject to speculative fluctuations.

- Allows additional planned development with the full consent of residents, providing affordable housing and a more livable environment.

- There will be a group of resident-shareholders focused on maintaining the value of all the properties owned by the corporation; setting quality controls.

Six Steps for Implementing the “Homeowners Lease-to-Equity” Program

There are six steps to implementing and maintaining a HEC program to save local homes from foreclosure, restore foreclosed homes to their original owners, and make affordable housing available country-wide in the future:

- Pass appropriate federal enabling legislation to allow tax-deductible payments of principal and dividends for Homeowners’ Equity Corporations.

- Form a “Community Auction Board” and pilot Homeowners Equity Corporations in each local community affected by the crisis.

- Gain access to the “discount window” of a regional Federal Reserve to finance the HEC’s purchase of foreclosed properties in a community.

- Obtain the properties, targeting properties where there has been a “deed in lieu of foreclosure.”

- Lease the properties back to the former owners or new tenants.

- Repay the acquisition loans, thereby enabling resident-shareholders to acquire shares in their Homeowners Equity Corporation through “lease-to-equity” arrangements.

Step I: Pass the Appropriate Enabling Legislation

The Homeowners Equity Corporation is the application of some concepts that have been in place for over a third of a century. Based on the same credit and tax principles governing Employee Stock Ownership Plans or “ESOPs,” the HEC is a way for homebuyers in default to buy their homes back by purchasing shares in the HEC with part of their rent payments. Resident-shareholders become owners of the corporation that owns their homes.

The ESOP has become the only economically feasible way open to most workers with little or no savings to purchase shares in the companies for which they work. With the goal of encouraging worker ownership of America’s productive capacity, retirement law thus allows companies to deduct payments of principal as well as interest on a loan used by workers to purchase shares through an ESOP. The law also allows a company to treat dividends as tax deductible if they are used to make principal payments or passed through the ESOP to the workers.

The idea behind the HEC is to allow similar treatment of principal payments and dividends for the HEC. It has long been the policy of the Federal government to encourage home ownership (the reason for the home mortgage interest deduction and the home loan guarantee program). The HEC will take the next logical step, and apply principles of corporate ownership long established in the business world to home ownership.

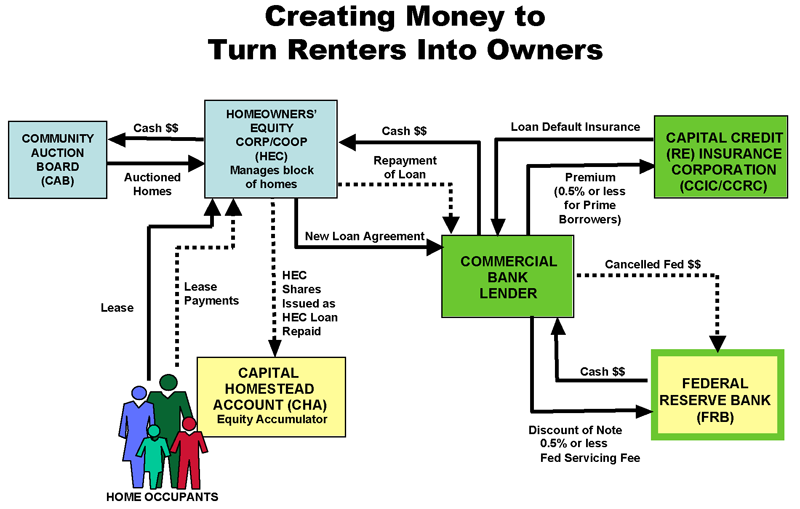

Step II: Form a Community Auction Board and Homeowners Equity Corporations

Homeowners’ Equity Corporations (HECs) would be set up as private sector holding companies to own directly residential structures now subject to foreclosure in a community, or that have been foreclosed and are owned by the mortgage companies, banks, or other financial institutions. HECs would obtain title to the homes, obtaining interest-free financing (described below) through local commercial banks. Eventually, HECs might develop or redevelop new residential structures, obtaining the properties and financing through local commercial banks that have access to interest-free money from a regional Federal Reserve Bank.

A HEC shareholder’s ownership stake in the value of his or her home leased from a HEC would be based on the number of shares issued. The number of shares, in turn, would be based on the negotiated price of the home at the time the HEC purchased it. Presumably this would be a price discounted from the original mortgage principal currently in default, and representing the actual fair market value of the home. The number of HEC shares, initially held in an escrow account as collateral for a new FHA-insured HEC mortgage, would be released to the HEC shareholder based on the number and amount of lease payments. Thus, ownership in a HEC would be based on pro rata contributions in the form of lease payments for the home occupied by the HEC leaseholder.

Every community with homes subject to foreclosure that will be acquired by the federal government or the Federal Reserve would establish a “Community Auction Board” (CAB). Each CAB would be chartered by the State government, and would have a balanced board of directors made up of leaders from the real estate industry, lawyers, accountants, and bankers. The CAB would hire or contract with professional auctioneers to determine the new fair market value of the loan in default through an open bidding process among competing HECs organized by local real estate management professionals.

The “winning” HECs would negotiate a new 100% leveraged loan to purchase the auctioned home mortgages with the commercial banks serving the community, with the acquired property serving as collateral at its real fair market value. The commercial bank would in turn bundle all HEC loans and sell them at the regional Federal Reserve’s discount window in exchange for new, asset-backed money. The cost of the loans to the HEC borrowers would be comprised of a service fee plus a risk premium.

Rental agreements would reflect the debt service costs, home mortgage insurance premiums, real estate management fees and profits of the HEC, plus any maintenance contracts with the renter of each home. This would allow the overall rent-to-equity process (auctions and real estate management functions) to be expedited efficiently at the community level rather than dealing with a bureaucracy within the national entity now holding the defaulted mortgage paper.

The benefit to the State, the Federal Reserve, and (especially) the taxpayer is that the State and the central bank would be able to unload the foreclosed properties quickly, and use the money-creation power of the Federal Reserve to keep most, if not all occupants in their homes. Due to the lower cost of the loans and the acquisition of the properties at a realistic market value, rent payments would be less than the mortgage payments they would otherwise have had to pay. Those families in need could be offered a sliding scale of rental vouchers in amounts necessary to make the new rental payments affordable, as under the Section 8 program of HUD.

To the extent such a strategy requires time to organize at the federal, state, and community levels, the Congress can pass a moratorium of 3-12 months on foreclosures of Federally-acquired mortgages in default while the HEC and CAB entities are being formed throughout the nation.

Once this program is up and running, the Congress can take steps to enact the Capital Homestead Act, which contains structural reforms to inhibit and, in most cases, prevent anything like the current crisis from happening again.

Step III: Gain Access to the Discount Window of a Regional Federal Reserve Bank

In order to make them financially feasible, HECs will need access to no-interest, low-cost financing sources, such as commercial banks with access to the Federal Reserve Discount Window. Regional Federal Reserve Banks have the power, under Section 13, paragraph 2 of the Federal Reserve Act of 1913, to discount through commercial member banks “qualified industrial, commercial, and agricultural” short-term loans. Although contrary to the original intent of the Federal Reserve, the Federal Reserve normally uses this power only to bail out member banks that are “too big to fail.” To this has recently been added the rescue of real estate speculators and investment bankers from the results of their own folly. An enabling amendment through the Congress might be necessary if negotiations with a regional Federal Reserve fail to allow the Federal Reserve to discount qualified loans for longer periods than currently permitted under the Act, restricting this longer term provision to loans extended through vehicles that broaden direct ownership of income-generating private property.

Step IV: Obtain the Properties

HECs would purchase foreclosed properties at a price discounted by the foreclosure situation, either through the homeowners or directly from the current mortgage lender/holders. The purchase of the properties would be financed with “new money” from the regional Federal Reserve, backed by the current market value of the houses and land and FHA or private-sector mortgage insurance. The HEC would assume the loan obligation and lease payments. In instances in which a tenant could not be found immediately for a property, a moratorium could be put on debt and lease payments until a tenant could be found, at least until the HEC has built up sufficient cash reserves to meet regular lease and debt service payments.

Where foreign investors have purchased bundled loans that include loans on homes in local communities, the HEC could offer these investors fair market value for those loans if they separate them from the others. A foreclosure would be expensive and get them much less, if anything.

Step V: Lease the Properties to the Former Owners or New Tenants

When a former owner or new tenant wanted to lease a house, the HEC would issue shares to the value of the leasehold, and put the shares in escrow. The HEC would gradually release shares from escrow to the leaseholder, as the HEC received enough money in the form of lease payments to repay the purchase loan. The former owner/now tenant would thereby build equity in the form of directly owned HEC shares. There would thus be an incentive for borrowers in danger of default or foreclosure to offer a deed in lieu of foreclosure to the lender, a process that must be voluntary on the part of the borrower.

In this way, homeowners or prospective homeowners who could not meet ordinary mortgage payments or qualify for a loan could, through the payment of rent, build equity not directly in the homes they rent, but in the company that owns the homes they rent. This is a more secure way of home ownership in some ways than the current arrangement. With a traditional 99-year lease, there would be little difference between a leasehold of this type (in which the tenants own the “landlord”), and directly-owned land and residence.

This would include any tenants receiving a rent subsidy in the form of a voucher, calculated on a sliding scale. It is irrelevant to the HEC where the money comes from to make a rent payment; each tenant will build equity in the form of HEC shares commensurate with the lease payments, not the source of the money used to make lease payments. A blanket waiver for having assets in the form of HEC shares will need to be issued for any HEC shareholder on welfare, exempting the shareholders from the usual requirement to be a pauper before receiving assistance.

Step VI: Repay the Acquisition Loans

The HEC would use the cash received as lease payments to retire its debt with the commercial lender (which in turn will purchase the debt paper back from the regional Federal Reserve). When a leaseholder makes lease payments sufficient to repay the HEC’s acquisition cost of the home, plus property taxes, maintenance, and a contribution to the cash reserves of the HEC (to maintain the properties and build up a repurchase pool), all shares would be released to the tenant and the lease payments reduced to a level sufficient to cover property taxes, maintenance, and the cost of any capital improvements made or paid-for by the HEC. That is, there would be no more payments on the mortgage, just a “pass through” of costs ordinarily borne by a direct owner.

All capital improvements (e.g., significant remodeling, new roof, add-ons, etc.) would be approved by the HEC. If the tenant pays for the capital improvement, he or she will receive HEC shares to the value of the capital improvement. If the HEC pays for the capital improvement and finances it with no-interest credit, shares will be put into escrow and released as the tenant makes lease payments. If the HEC pays for the improvement out of the maintenance fund, no shares will be issued.

It may be politically expedient at present to provide for the sale of the home to a leaseholder who pays off the acquisition cost of the property. This could be done by exchanging the tenant’s HEC shares for the deed to the house. Lease payments and all other costs, such as maintenance and property taxes, would become the responsibility of the new owner/former tenant. If adopted, this provision should have a sunset date, or deeds could be covenanted to allow for the purchase of the land (not the structure) by a Community Investment Corporation, should such a vehicle be implemented in a country or region, and leaseback by the owner of the house.

Conclusion

The home mortgage crisis can be solved in any local community by structuring home ownership in the form of directly-held equity shares in a real estate holding company that owns the homes rented by the shareholders, and financing the HEC purchases of these properties through the Federal Reserve.

This concept paper presents a solution that will not force taxpayers to foot the bill for a temporary and extremely ephemeral “stay of execution” in the form of a massive, Federally funded bailout of predatory lenders that puts off foreclosures for 30 days and leaves the basic problem untouched. Further, by creating a replicable exemplar in a local community, other communities will have a model for a permanent, financially sound, and politically feasible solution to the current sub-prime mortgage crisis. Such an approach can grow organically, strengthening local communities and their residents, and thus preventing future crises from developing.

Finally, this proposal has the potential to begin the process of stabilizing the U.S. dollar and providing a model for encouraging the use of the Federal Reserve discount window for qualified industrial, commercial, and agricultural loans, and wean the government off its dependence on non-productive debt instead of the tax base.

America’s foreclosure crisis offers a unique opportunity for local communities and the nation as a whole. With new ideas like the Homeowners Equity Corporation, we can take one part of the American Dream — home ownership — to the next step, economic independence through ownership of productive capital through a “Capital Homestead Act.”

112513